One of the biggest problems with value is the time it takes to work itself out. Over, and under valued securities and markets can stay stubbornly mispriced for years, or even decades. My favorite grandaddy of all bubbles, Japan, took about 20 years to get back to normal valuation. And even now the stock market is down 30% from all time real highs (including dividends).

One popular criticism of the valuation models that Hussman, Gray, Buffett, Shiller, Grantham, and Philbrick et all propose is that they tend to work over 5-15 years. Many conclude that they are then worthless as most people are trading on shorter time frames etc. It doesn’t matter if it is PE, CAPE, Tobin’s Q, dividend yield or mkt cap to GDP, most don’t work that great in the short term.

(Note: Our Global Value paper introduces another element, and that is relative valuation, which was shown to work great on much shorter time frames.)

So what is a simple answer to this criticism? Simple: hold the position longer.

Below we set out to test a very simple system. The goal is to have a maximum allocation at cheap secular lows, and a minimum allocation at secular, expensive highs.

We divide the portfolio into five buckets of 20% each. Each bucket can be anywhere from 0-100% invested in stocks, and the remainder is in 10 year bonds. Therefore, the entire portfolio can be 0-100% invested in stocks or bonds.

Rules:

Each year only update one bucket.

If CAPE < 10, 100% of that bucket is in stocks. 0% in bonds. Hold that position for 5 years.

If CAPE < 15, 75% of that bucket is in stocks. 25% in bonds. Hold that position for 5 years.

If CAPE < 20, 50% of that bucket is in stocks. 50% in bonds. Hold that position for 5 years.

If CAPE < 25, 25% of that bucket is in stocks. 75% in bonds. Hold that position for 5 years.

If CAPE > 30, 0% of that bucket is in stocks. 100% in bonds. Hold that position for 5 years.

Next year, repeat with the next bucket, so that each year you are updating just 20% of the portfolio (talk about lazy portfolios!)

(Note: These cutoffs and % were picked out of a hat. I’m sure there are better parameters, such as holding for 7-10 years.)

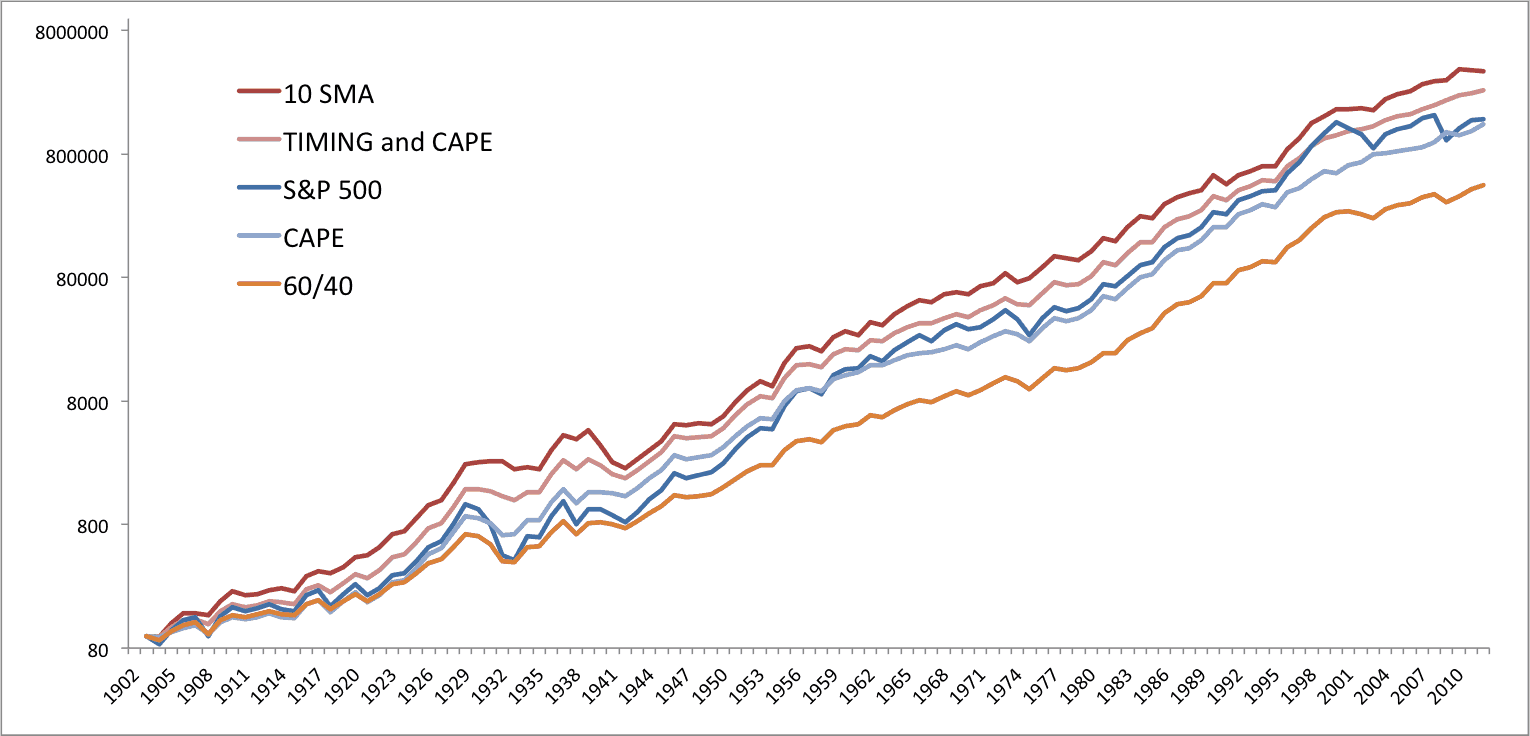

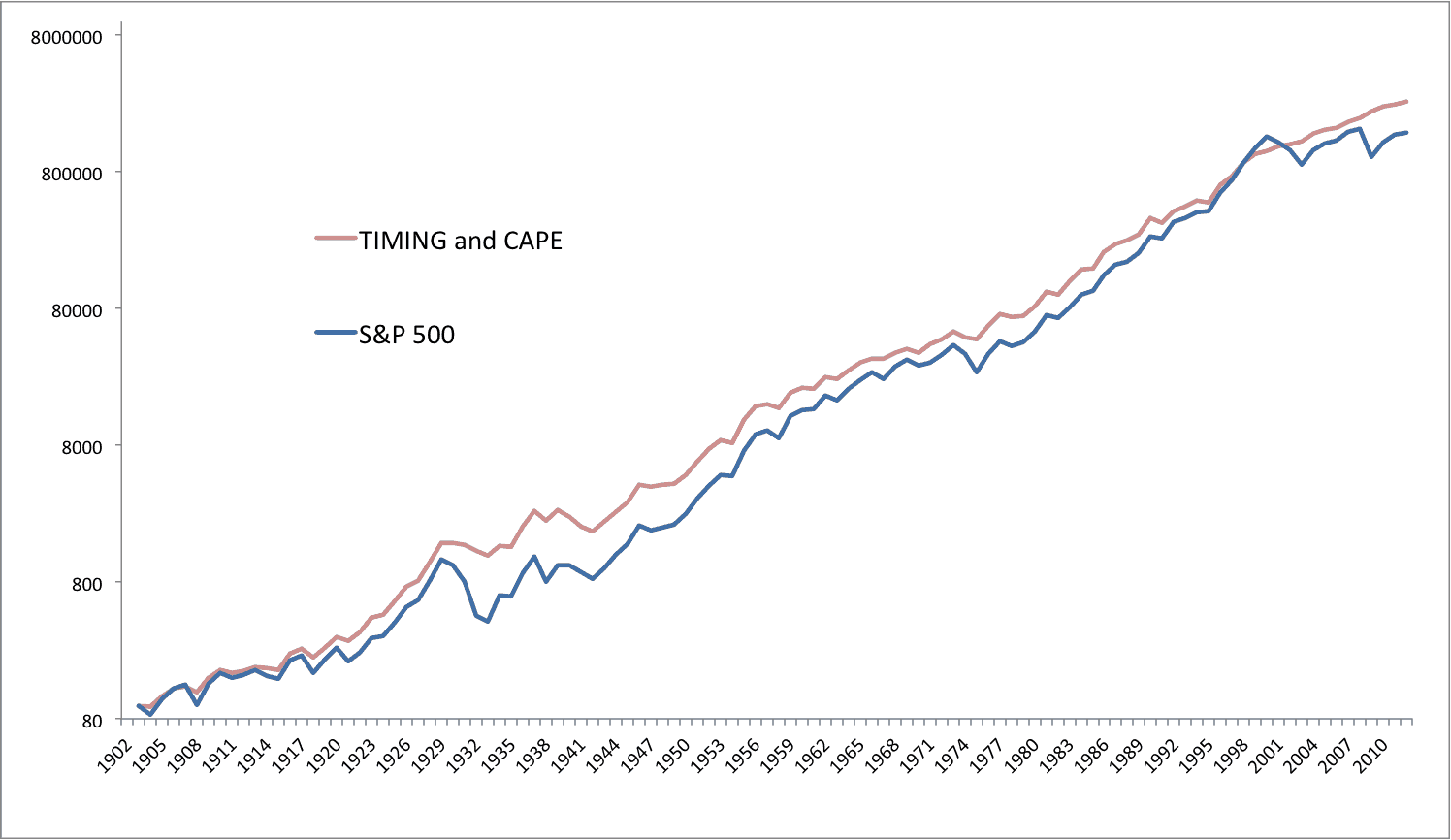

This way you have a portfolio that matches the holding period with the intended indicator horizon. More importantly, how does it work? (CAPE is the above strategy, not the CAPE strategy from the paper. 10 SMA is the moving average model from our QTAA paper. )

Not bad – nice reductions in volatility and drawdowns. I’m sure you could tweak the parameters with longer holding periods as well as better CAPE cutoffs, as well as even potentially using leverage and shorting. Even better would be to use all of the global markets instead of just one.

Will try and write up in a longer paper at some point…readers, feel free to play around with the Shiller data on your own and report back!