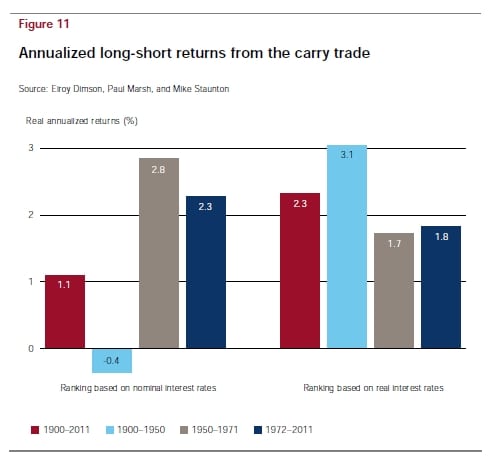

There is ample research that shows that sorting government bonds on yield works great. The outperformance has been very consistent over the years at about 2% a year. The Dimson, Marsh, Staunton crew examined this in their 2012 GIRY issue, and graphic is below. These are returns from going long high yielding and short low yielding countries, but one issue with that strategy is that the drawdowns are approx double what you would find in the long only side of the portfolio.

So we went back to 1900 with over 30 countries with data from GFD. (There were almost 20 countries with bond data back to the 1920s.) Not surprisingly, the returns hold up well with the expanded universe.

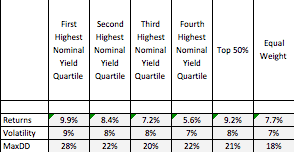

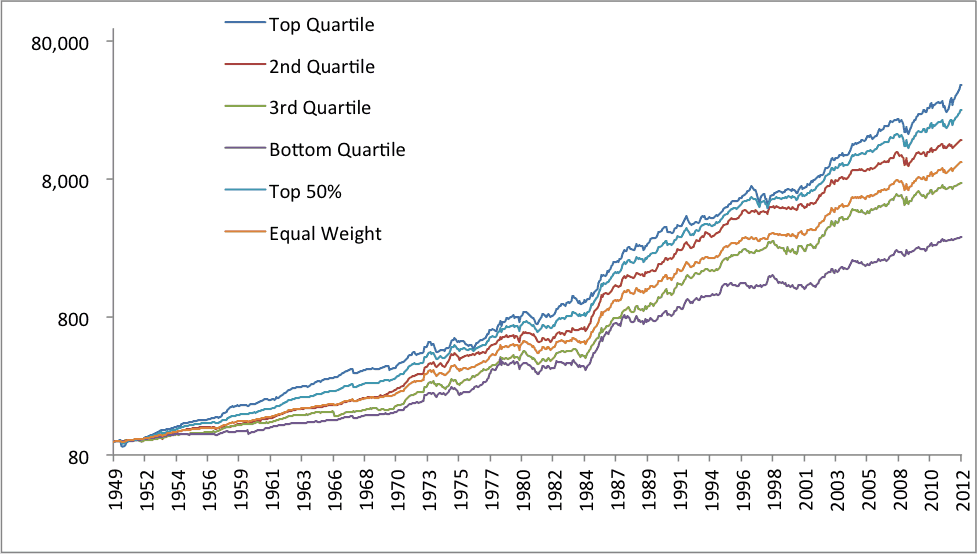

For a more recent view, below are the results to 1950. Roughly 2% outperformance that is consistent across decades. These are USD unhedged returns though we have tested it both ways (the above DMS study is local real returns). I like to describe this not as “buying the highest yielding bonds”, but rather, “avoiding the lowest yielding bonds”.