Cambria Fund Profile Series – Cambria Asset Allocation ETFs (GAA) (GMOM) (TRTY)

![]()

![]()

![]()

![]()

![]()

Host: Meb Faber is Co-Founder and Chief Investment Officer of Cambria Investment Management. Meb has authored numerous books, whitepapers and blog posts, and is the host of The Meb Faber Show podcast.

Date Recorded: 10/22/2020 | Run-Time: 20:24

Summary: In today’s episode of the Cambria Fund Profile Series, Meb discusses Cambria’s Asset Allocation ETFs, the Cambria Global Asset Allocation ETF (GAA), the Cambria Global Momentum ETF (GMOM), and the Cambria Trinity ETF (TRTY).

Meb kicks off the episode with the advantages of holistic-all-in-one asset allocation portfolios. He talks about the classic 60/40 portfolio balanced between stocks and bonds, and some of the potential drawbacks to that approach given the state of valuations in both markets right now. He discusses how investors can break out of the 60/40 model, and offers what he feels is a proper approach to building a globally diversified portfolio of assets.

He walks through each of Cambria’s asset allocation funds, the thinking behind each, what each fund brings to the table, and the challenges each fund sets out to tackle for investors.

All this and more in this Cambria Fund Profile Series episode, featuring Cambria’s asset allocation ETFs, (GAA), (GMOM), and (TRTY).

Comments or suggestions? Email us Feedback@TheMebFaberShow.com or call us to leave a voicemail at 323 834 9159

Interested in sponsoring an episode? Email Justin at jb@cambriainvestments.com

Links from the Episode:

- 0:34 – Intro

- 1:45 – Holistic, globally balanced portfolios

- 3 :10 – Building a diversified portfolio

- 4:09 – 60/40 portfolio drawbacks

- 4:18 – 60/40 portfolio historical performance

- 4:45 – US stock valuations

- 5:18 – Status of US bonds

- 5:44 – Global Investor Study (Schroders)

- 6:08 – Expanding on a US focused portfolio with a global asset allocation

- 6:50 – Cambria Global Asset Allocation ETF (GAA)

- 7:38 – Global Asset Allocation (Faber)

- 8:51 – Asset Allocation Portfolios Updated Through 2019

- 9:02 – Impact that fees have on investment results

- 10:10 – GAA factor tilts

- 11:30 – Cambria Global Momentum ETF (GMOM)

- 13:52 – Cambria Trinity ETF (TRTY)

- 13:59 – Big picture – buy and hold vs. active, tactical traders

- 15:26 – Finding a middle ground

- 17:41 – Disclosure

Transcript:

Welcome Message: Welcome to The Meb Faber show where the focus is on helping you grow and preserve your wealth. Join us as we discuss the craft of investing and uncover new ideas, all to help you grow wealthier and wiser. Better investing starts here.

Disclaimer: Meb Faber is the co-founder and chief investment officer at Cambria Investment Management. All opinions expressed by podcast participants are solely their own opinions and do not reflect the opinion of Cambria Investment Management or its affiliates.

Intro: Howdy podcast listeners, we have a little bit of a different show for you today. Over the past decade, we’ve made an effort to educate our clients and investors, now over 40,000 strong, by publishing research and commentaries across the blog, academic papers, books, speeches, and now in the more modern social world, Twitter, YouTube, and this podcast. However, we still get many great questions every day about our funds, many of which are broadly similar, so we wanted to try and use this platform to help educate shareholders as much as possible. You know, Sometimes the spoken word provides a little more context and narrative than just an academic paper or factsheet. And as always, the most important thing in investing is finding an approach that works for you, which may or may not involve any of our funds, which is totally fine. We just want our shareholders to be as informed as possible in what they’re invested in. So enough intro, please enjoy today’s episode in our series of fund profiles.

Welcome, friends. Today, we have a special episode which, in my opinion, reduces to one, powerfully-important influence on whether or not you reach your investment goals – simplicity.

As part of this, we’re going to discuss three Cambria funds that, we believe, are one-and-done investments. And what I mean by that is we think each fund offers investors a holistic, globally-balanced portfolio – with the benefit being that these entire portfolios come wrapped in the convenience of a single ETF.

Each fund does all the heavy lifting of rebalancing, tax harvesting, and moving in a out of positions for you. Again, they’re basically holistic portfolios, wrapped into a single investment. So, you make an initial allocation and you’re done. Continue adding deposits as you like, and simply let time compound for you.

Now, these three funds share many similarities, which we’ll discuss today. The difference between them lies in their specific philosophies and implementation tweaks, which impacts their return-paths and their volatility. An investor’s specific risk/return preferences will impact which fund is the best choice for them.

So, today, let’s look at the Cambria Global Asset Allocation ETF (ticker symbol GAA), the Cambria Global Momentum ETF (ticker symbol GMOM), we call it GMOM, and the Cambria Trinity ETF (ticker symbol TRTY). We believe that each one provides investors with a simplistic, one-click way to own a powerful, holistic portfolio. The idea being that each fund offers a chance to generate long-term returns that make a real difference in wealth, while producing less anxiety during periods of heightened market volatility and drawdowns.

Let’s jump in.

So, when it comes to building a portfolio, you can argue that the granddaddy of them all is the 60/40 portfolio, which is 60% in US stocks and 40% in US government bonds. The intended benefit of diversifying into two asset classes is the hope that these assets may zig and zag, where both investments perform well over time, but not necessarily always at the same time.

The combination of the two will hopefully protect your portfolio more from losses and drawdowns than investing in one asset alone. This is important since massive drawdowns are often an experience most investors can’t handle psychologically – many of us think we can handle them until they’re actually eroding our portfolio value. And to make sure we’re on the same page, we define a drawdown as a peak to trough monthly loss, so if an $100k investment and it declines to $70k on its way back up to $200k, that at one point was a 30% drawdown.

Now, while historical studies show that having two asset classes does tamp down portfolio volatility from a “just stocks” level, the 60/40 portfolio does have its drawbacks – namely, what if one of those two assets underperforms? What if both assets do poorly at the same time?

If we run a historical test on a U.S.-based 60/40 portfolio with data dating back to 1926, you’ll find that even with lower volatility than just stocks alone, the 60/40 portfolio still had a whopping drawdown of over 50%! Plus, with just two assets, the 60/40 portfolio’s future returns are especially sensitive to each asset’s starting valuation. In other words, the price you pay influences your rate of return in the future.

And as I’m recording this, U.S. stocks are among their highest valuations ever as measured by the 10-year cyclically adjusted price to earnings ratio (also known as the Shiller CAPE Ratio). Currently, US stocks trade at CAPE ratio of 32, vs a historical norm of about 17. Even if we give an allowance for the low-inflation environment of the past 40 years, the average CAPE value only climbs a little higher to 22, clearly still well-below our current reading of 32. So from a historical standpoint, that doesn’t bode well for the next decade’s worth of returns.

And we all know where U.S. bonds stand. With the U.S. 10-Year-Treasury yielding less than 1%, and negative when we adjust for inflation, they’re unlikely to contribute much to total returns.

So, we have historically high stock valuations combined with historically low bond yields. Though there are no crystal balls with investing, this doesn’t look that good for robust returns this coming decade.

Of course, that’s not what investors think.

A recent Schroders study of US investors found that annual return expectations were over 15%! Yikes.

While those returns would be wonderful, history suggests investors might be getting a little bit ahead of themselves.

I’m quoting an April 2020 investment survey from Schroders that puts it simply: “People are over-optimistic about their investment returns over the next five years.”

Yah think?!

So, what might be a more of a balanced approach to a portfolio than expecting blockbuster returns from only U.S. stock and bonds?

Well, why not go global and add more asset classes?

By diversifying away from holding just one country, we greatly increase the odds of protecting ourselves from outsized losses, which is huge – just ask an investor in Brazil, Greece, Russia, or many other countries over the past few years!

And by also adding additional asset classes beyond just stocks and bonds, historical data suggest this will help us squeeze every bit of return out of the degree of risk we’re willing to accept.

The specific asset classes we’re going to add here are commodities and real estate – we’ll be using publicly traded REITs for real estate exposure.

This brings us to the first Cambria fund we’ll discuss today – the Cambria Global Asset Allocation ETF, with the ticker GAA.

In essence, GAA resembles the portfolio you would own were you to wrap all global public investments into one, composite portfolio – often described as the “Global Market Portfolio”.

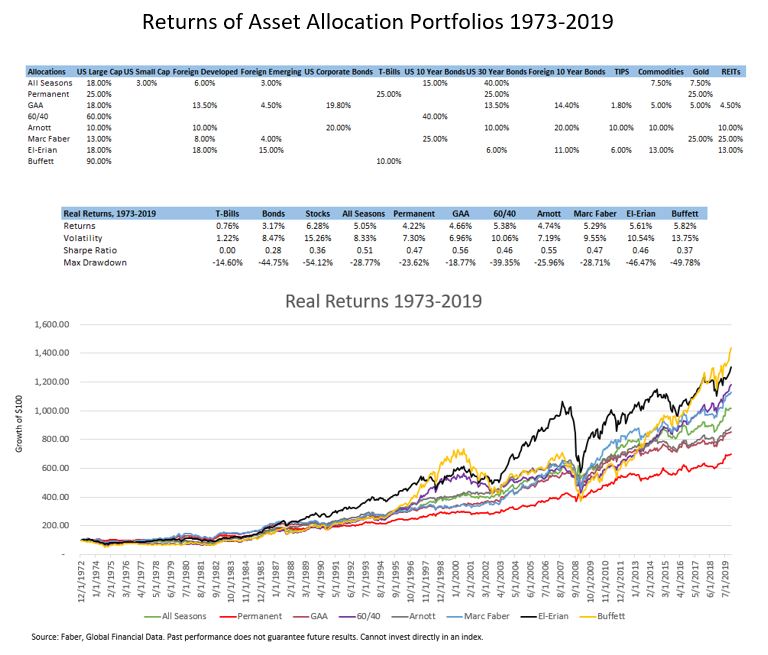

In our book Global Asset Allocation, which by the way is free to download on our website, we examined the hypothetical performance of the global market portfolio strategy from 1973 through 2013, and found that it produced greater returns than a 60/40 portfolio – and that includes both a U.S.-focused and global 60/40. Plus, it did this while lowering volatility.

Now, some listeners may be thinking “so you just own the world? Certainly, the big-name money managers would crush this type of global portfolio from a return-perspective.”

And for anyone thinking that, lemme share something that’s likely to surprise you.

Again in my book Global Asset Allocation, we studied the historical returns of buy-and-hold and rebalanced asset allocation portfolios suggested by some of the brightest minds in investing, including Warren Buffett, Ray Dalio, Mohammed El-Erian. I also included well-known allocations like Harry Browns’ Permanent Portfolio. We examined the historical simulated returns of these asset allocation models from 1973-2013.

These various portfolios contained a total of 13 different asset-class building blocks. But an investor could simplify and reduce them to three broad categories: global stocks, global bonds, and global real assets.

As part of this study, we compared these portfolios to our Global Asset Allocation approach.

And what we found was truly remarkable…

Even with the difference in allocations, the annual compound return spread between the worst-performing allocation, over that period, and the best performing allocation, was less than 2 percentage points.

That similarity of returns is astonishing and points toward what we believe is an important takeaway:

With a long-term investing timeframe, as long as you have the right, main ingredients—so, some global stocks, bonds, and real assets— we believe you’re going to end up in the right ballpark.

On a side note, we’re also proud to report that the global market portfolio approach came in among the highest returns with among the lowest volatility levels. But we’ll also put those results in the show-notes too.

So, to someone thinking that the long-term returns of a global market portfolio would get crushed by a big-name money manager, we’d answer “well, that’s not what our studies show.”

Given this, when you have the right, main ingredients, what we think is vastly more impactful on your returns comes from somewhere else…

Fees.

Specifically, how effective you are at keeping your investment fees low.

Over the long-term, paying upwards of 1% or more in expense ratio fees can kneecap your returns. Depending on the size of your investment, this can amount to – literally – hundreds of thousands of dollars or more over the decades.

And that’s why we’re proud to offer the Cambria Global Asset Allocation ETF for a 0% management fee. To be clear, GAA is a fund-of-funds that owns other underlying ETFS. That means investors will pay the acquired fund fees, so right now around 0.37%, but given that Cambria doesn’t charge any management fees, the total fee for the ETF remains just 0.37%.

So while adding more global asset classes and paying low fees seems good theoretically, what if much of the traditional market cap weighted stock indexes around the globe are expensive?

What if most government bonds have zero or negative yields?

In those situations, how would going global be any better than sticking with the good ‘ole 60/40?

Well, it probably wouldn’t be over the long-term.

And that’s where value comes into play.

So, in GAA we start with the global market portfolio, but then we tweak it a bit.

Specifically, we add overlays to our core investment set. Some investors may call these factor tilts.

While we utilize multiple tilts in the portfolio, as an example, let’s discuss a tilt many are familiar with – value.

A value-tilt simply means we’re investing more heavily in global stocks exhibiting traditional traits of being priced at low valuations.

But it’s not just stocks. We also tilt toward value in the bond world. We do this by moving away from the market cap weighted index, where about 70% of the global debt comes from only five countries, many of which are trading at negative yields! Instead, our global value methodology invests in the highest yielding sovereign bonds around the world.

Now, before we move on from this point, think about why a value-tilt helps.

Our historical research suggests going global with a value tilt increases returns. But again, it’s not just about investing in what’s least expensive, it’s also important to avoid what’s expensive…

And as we noted earlier in this podcast, future returns are often inversely-correlated to starting valuations.

So, pulling back big-picture for a moment. To us, GAA represents a perfectly suitable long-term market approach, consisting of the basic building blocks of a globally-diversified portfolio, with tilts to factors like value, all offered with a low, all-in expense ratio.

So now, let’s move on to the next evolution of this portfolio – the Cambria Global Momentum ETF, with the ticker, GMOM, GMOM.

Like GAA, GMOM starts by considering a similar universe, that being a wide array of assets from all over the globe. And given its engineering, GMOM will allocate to some funds with factor tilts, so GMOM can skew to areas like value too.

But GMOM differs quite a bit from GAA in that it uses a tactical overlay focused on “momentum” and then “trend.”

The fund does this with the intent of improving overall risk-adjusted returns, with a focus on avoiding long bear markets. After all, bear markets can be hard on an investor psychologically, leading to emotion-based investment decisions that often derail long-term goals.

So, Specifically, GMOM targets the top third of investments in its broad universe of potential funds every month, selects the investments displaying the greatest short-to-long term trailing momentum.

And now, in short, the reason we do this is because historical market data suggest that investments with strong momentum tend to continue moving in the direction of that momentum.

Of course, momentum goes both up and down. GMOM seeks investments that are only going up. So, this is where we bring in the second tilt toward trend. And in this case, that’s an upward trend.

GMOM uses a long-term trend following indicator to ensure that the holdings are in an uptrend. And if a selected holding is in a downtrend, that allocation moves to cash or bond ETF replacement.

So, as to the benefit of these tweaks over GAA, past research we’ve performed shows that, historically, sorting assets based on trailing measures of momentum and trend has led to better risk adjusted returns.

We believe GMOM offers a balanced approach to the markets that gives investors exposure to must-have portfolio assets, while benefiting from the overlays of momentum and trend.

A question you might have at this point, which we’re often asked is “which strategy is better between GAA and GMOM?”.

Our answer is “well, you know, we love all of our children!”

But more importantly, we’re not in a position to tell any specific investor what’s better for him and her without understanding their unique financial situation and goals.

So, we can’t comment on “better” or “worse.”

But we can say that the big difference between the two funds is mostly philosophical. We believe that both funds will do well over time, but their respective performance paths will likely zig and zag during many different market regimes.

And that leads us to the final fund we’ll discuss today, the Cambria Trinity ETF, with the ticker TRTY.

So, let’s go big-picture for a moment.

Most investors tend to fall into either one of two groups: buy-and-hold, or, an active, tactical trader. Both approaches have their pros and cons.

For example, buy-and-hold can be great with a quality investment over the long-haul – but only if you’re willing to be able to stick your head in the sand during pullbacks of 20%, 30%, 50%, or even more – which many investors can’t do.

Lots of people struggle with buy-and-hold when it’s hitting the fan and markets are declining – think back to the Global Financial Crisis, or even a few months ago. We’ve spoken to lots of investors that “couldn’t take it anymore” and sold everything, never again to reinvest. Think about the gains they’ve missed over the past decade.

On the other hand, tactical trading, like trend following, can be great when it helps investors sidestep big drawdowns. But then again, market studies suggest that most active traders underperform a long-term buy and hold strategy. That’s because it’s really hard, if not downright impossible, to properly time the highs and lows of the markets with regularity.

The idea of market-timing comes into play when we’re talking about the tilts of momentum and trend. That’s because market-timers try to find their entry and exit points by using various momentum and trend filters.

Sometimes these can work great, but other times they’re not-so-great. When markets are choppy and moving sideways, a momentum and trend approach can underperform a buy-and-hold allocation.

The point is tactical trading can be challenging for investors too, just like buy-and-hold. After all, it’s really hard to be horribly underperforming your neighbor.

Given this, we thought about how to find a middle ground. We wanted to give investors the peace that comes with knowing that a portion of their portfolio is benefitting from whatever market dynamic is prevalent at that moment – whether that’s buy-and-hold, or momentum and trend.

And that’s the mindset we had when constructing our Trinity ETF.

Like the other funds, we started with globally diversified assets with factor tilts. But when it came time to decide between buy-and-hold versus momentum and trend, we took a different approach.

We went halfsies – very technical term, I know.

Specifically, Trinity invests roughly half into a global buy-and-hold portfolio with tilts as our foundation – basically, the GAA strategy. But then, with 50% of this portfolio to a global trend strategy as well, making that part resemble the GMOM strategy.

We believe the main benefit of this 50%/50% approach boils down to one thing – psychology.

It’s hard for most investors to underperform a benchmark, an index, or again, your neighbor – especially your neighbor. Given this, we believe that the best market strategy isn’t necessarily the one that looks the best on paper – which, many times, is the one that makes you sit through huge drawdowns – it’s the one that an investor can stick with, year-in and year-out.

We think the Trinity ETF, with its exposure to both buy-and-hold and trend, reduces the chances an investor will jump ship. Again, that’s because part of the portfolio will likely be benefitting from either buy-and-hold or trend, or both.

So, that wraps up our overview of these three funds.

We believe each offers investors a one-click way to own a globally-diversified, portfolio investment. In our opinion, it’s investing made simple.

As we noted at the top of this podcast, each ETF is set-it-and-forget-it, meaning you don’t have to worry about rebalancing or moving in or out based on signals, because the underlying mechanics of the ETFs do it for you. You allocate your funds, then simply let the ETF do the rest.

And given how each one is engineered to follow different return-paths over the years, we’re confident that one of them will be able to suit your needs.

If you’re interested in learning more about any of these Cambria ETFs, or discussing which fund might be the best fit for you or your clients, you can visit CambriaFunds.com or reach out directly at 310.683.5500 or email us at info@cambriainvestments.com info@cambriafunds.com.

Thanks for listening, and good investing,

Disclaimer:

To determine if this Fund is an appropriate investment for you, carefully consider the Fund’s investment objectives, risk factors, charges and expense before investing. This and other information can be found in the Fund’s full and summary prospectus which may be obtained by calling 855-383-4636 or (ETF INFO) or visiting our website at www.cambriafunds.com. Read the prospectus carefully before investing or sending money.

The Cambria ETFs are distributed by ALPS Distributors Inc., 1290 Broadway, Suite 1000, Denver, CO 80203, which is not affiliated with Cambria Investment Management, LP, the Investment Adviser for the Fund.

A Few Definitions:

Shiller CAPE Ratio: The cyclically adjusted price/earnings ratio is the price of a security of equity index divided by the average inflation-adjusted earnings over the past 10-years.

GAA seeks income and capital appreciation.

GMOM seeks to preserve and grow capital from investments in the U.S. and foreign equity, fixed income, commodity and currency markets, independent of market direction.

TRTY seeks income and capital appreciation.

GAA, GMOM, and Trinity are actively managed.

Past performance is not indicative of future results

GAA and Trinity’s investment objective and strategy changed effective January 1, 2019.

Shares are bought and sold at market price (closing price) not net asset value (NAV) are not individually redeemed from the Fund. Market price returns are based on the midpoint of the bid/ask spread at 4:00 pm Eastern Time (when NAV is normally determined), and do not represent the return you would receive if you traded at other times. Buying and selling shares will result in brokerage commissions. Brokerage commissions will reduce returns.

There is no guarantee that the Fund will achieve its investment goal. Investing involves risk, including the possible loss of principal. In addition to the normal risks associated with investing, international investments may involve risk of capital loss from unfavorable fluctuation in currency values, from differences in generally accepted accounting principles, or from social, economic, or political instability in other nations. These risks are especially high in emerging markets. Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. Investments in commodities are subject to higher volatility than most traditional investments. The fund may invest in derivatives, which are often more volatile than other investments and may magnify the Fund’s gains or losses. The use of leverage by the fund’s managers may accelerate the velocity of potential losses. The Fund employs a “momentum” style of investing that emphasizes investing in securities that have had higher recent price performance compared to other securities. This style of investing is subject to the risk that these securities may be more volatile than a broad cross-section of securities or that the returns on securities that have previously exhibited price momentum are less than returns on other styles of investing or the overall stock market. Investments in smaller companies typically exhibit higher volatility. Diversification may not protect against market loss. There is no guarantee dividends will be paid.

The funds are actively managed using proprietary investment strategies and processes. There can be no guarantee that these strategies and processes will produce the intended results and no guarantee that the Fund will achieve its investment objective. This could result in the Fund’s underperformance compared to other funds with similar investment objectives.

CBM000322

{kind=link}