This excerpt is from the book Global Asset Allocation now available on Amazon as an eBook. If you promise to write a review, go here and I’ll send you a free copy.

—-

Larry Swedroe is one of my favorite writers and researchers. With 15 books to his name, his focus on evidence based investing fits in well with how we view the world. We debated about including this portfolio in the book since it requires using a value tilt, but think it is an important example of how a simple smart beta strategy may be beneficial to the overall portfolio.

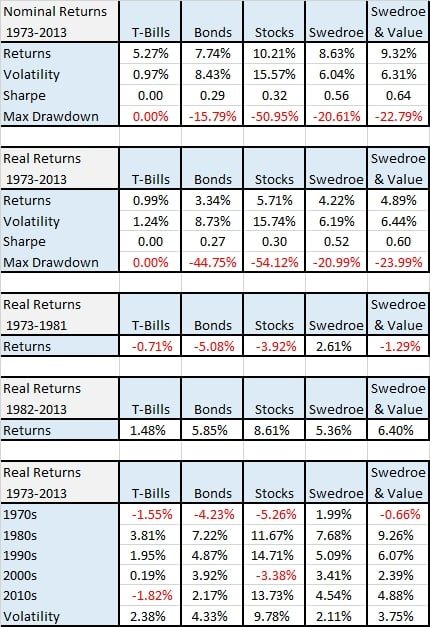

The biggest difference between the allocation and others in this book is that he allocates to small cap value. Small cap value stocks have outperformed broad small caps by about four percentage points a year, which is a lot. The value stocks have slightly more volatility and a higher drawdown as well.

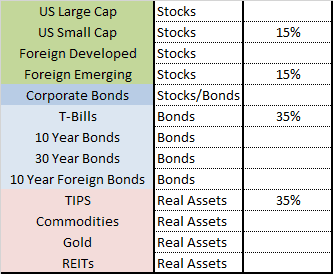

FIGURE 57 – Larry Swedroe Eliminate Fat Tails Portfolio

Source: Swedroe

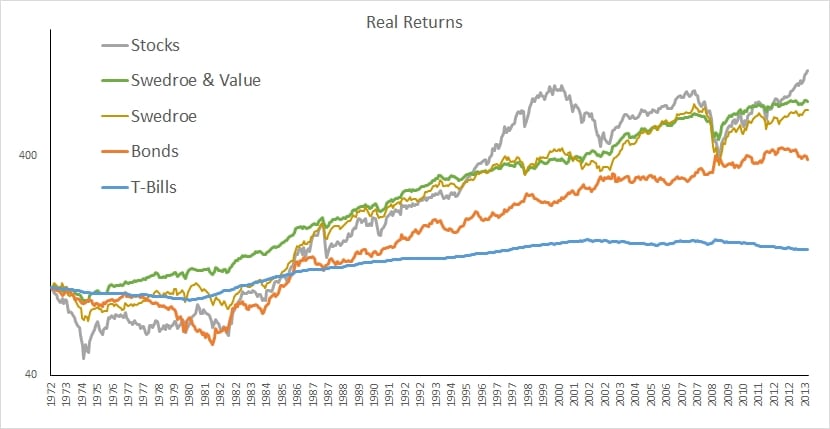

Below are the portfolios returns for comparison.

Swedroe’s unusual allocations are another example of a consistent performer due to including a mix of stocks, bonds, and real assets. We include the performance of including small cap as well as small cap value to illustrate the improvement in performance. The portfolio with the value tilt results in the highest Sharpe ratio of any portfolio in the book.

FIGURE 58 – Asset Class Returns, 1973-2013

Source: Global Financial Data