South Park is an award-winning, animated TV show on Comedy Central.

In one particular episode, we’re introduced to Ms. Claridge, an invalid who communicates only through a series of computerized beeps. One beep means “yes” and two beeps meaning “no.”

There’s a scene in which an accident leads to several buildings burning down. Everyone believes the culprit is the local deviant, Trent Boyett. But the reality is Trent had nothing to do with it.

Because Ms. Claridge witnessed the accident, a cop asks her, “Did Trent Boyett start the fire?”

Ms. Claridge responds with two beeps (which means “no.”) But the interviewing cop, already completely convinced that Trent Boyett was to blame, turns to his fellow police officers and says someone along the lines of “You heard her, Boys – she said ‘yes, yes!’ Take that troublemaker Trent Boyett downtown!”

How often do we do something similar when it comes to investing?

Clear facts can be right in front of us, but because they’re not the facts we want to see, we simply ignore them. Instead, we remain fixated on our own market narrative, rejecting anything that challenges our investing thesis.

The term for this is “confirmation bias.” In essence, it’s the tendency to interpret or spin any new evidence in a way that confirms or supports your pre-existing belief or theory. The best analysts and portfolio managers in the world are relentless in seeking out information that questions their analysis, rather than just supports their dear beliefs. Think of the permabears and bulls on CNBC, that despite all contrary evidence will never change their minds. (Or a more apt analogy would be politics, with people only existing in an echo chamber that supports their political ideology.)

As investors, it’s critical that we all be aware of the extent to which we’re clinging to our market narratives out of blind loyalty – despite evidence to the contrary. Otherwise, market conditions could be clearly signaling “no!”, yet our biases have us stubbornly clinging to “yes, yes!”

I was recently reminded of this two weeks ago after being a guest on a panel, which featured the topic of “active versus passive investing.” Interestingly, my experience became very personal, as you’re about to see.

The active versus passive investing panel in which I participated was part of the UCLA Anderson Fink conference. Normally I would rather take a penalty kick to the face than debate this topic again, but I think UCLA does a good job with the conference and I wanted to give back and participate (some old posts on the subject: “Active Management“, “Let’s Bury Active vs. Passive“, “4 Lessons from RWM Conference“).

On the panel with me were two investment professionals that I’ve known for a long time, Mark Hebner of Index Fund Advisors, and Josh Emanuel of Wilshire Associates.

Mark and I tend to see the investing world somewhat differently. Some of those differences came to light during our panel discussion (you can watch the whole thing below).

While I left that panel that afternoon thinking the whole debate was over, Mark did not. He and his co-worker Tom Allen, wrote a follow-up article focusing on me and my firm, Cambria, generally casting our strategies and firm in a somewhat negative light.

The problem is that the article is so overflowing with Mark’s personal confirmation biases – so rigid in its investing worldview – that I’ve been scratching my head as to how two professionals as tenured and intelligent as Mark and Tom could write it. What I do know is that their article is a superb example of ignoring certain realities, and instead, clinging to a pre-existing narrative.

So let me state up front what I believe to be Mark’s central narrative, to which he’s clinging despite facts. Then I’ll lay out those facts, and you can decide for yourself.

I believe Mark sees passive, buy-and-hold investing as the holy grail of investing. But not just that, it seems he feels passive, buy-and-hold investing is easily definable and “pure” in a sense (I’ll explain more in a moment). Given this belief, Mark seems to feel that anything resembling “active” investing is inferior and more than likely, plagued by high fees compared to passive investing. Finally, it seems Mark’s narrative is that Cambria is an active shop, marketing only active funds, and therefore, we must fall into the “bad” camp, charging higher-fee products/services.

Let’s look at these biases now…

The first one I’d like to address is this notion of “passive buy-and-hold investing” is the best investing style – and not only that, but passive buy-and-hold is easily definable and pure in its nature.

The problem with this narrative is that, while it was perhaps once true – or partially true – it’s difficult to still make that argument.

You see, indexing used to mean something when it was introduced in the 1970s. It meant rules-based, low-cost, market cap investing. And that’s it. But over the years, the term has become so diluted and bastardized, today it is almost a phrase with no meaning. That “purity” of the early years is quite muddled now.

My example from the panel is The Cheeseburger Index (minute 4:30 to 7:00). You could create an index with these rules: Sort companies by CEOs who prefer cheeseburgers over hamburgers and equal weight the cheeseburger managers. Voila! You’re an index manager! It is a good investment idea? Most likely not, unless it turns out that there’s an amazing correlation between brilliant CEOs and a preference for cheese…

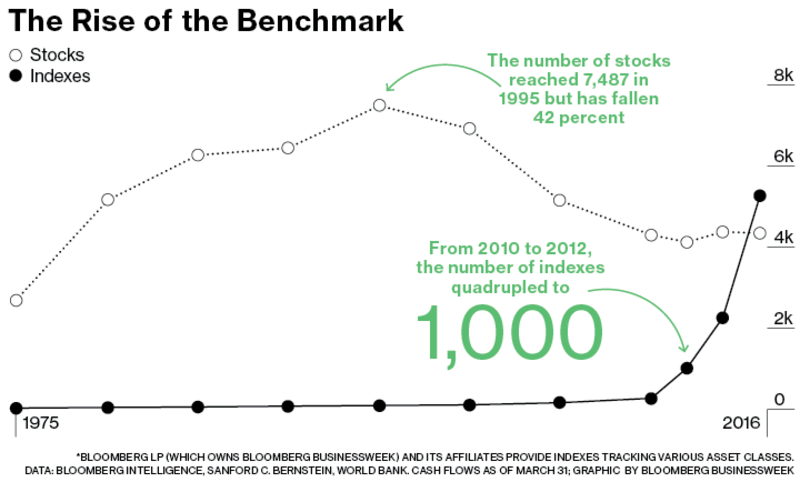

So, in addressing confirmation bias #1, note the absurdity of the “passive index” I just created. Just because it’s a passive index does not mean it’s a worthy investment. The Cheeseburger Index checks the box definitionally, but fails any reasonable common sense test. So already, blind allegiance to passive, buy-and-hold investing faces a problem – namely, so many things can be thrown into that category these days that is doesn’t really mean what it used to. Indeed, so many people have jumped on the passive index bandwagon that there are now more indexes than stocks!

As professional money managers, it’s important we recognize this, and evaluate the investment itself – not the alleged category that the investment falls into. But let’s take it to the next level…

What if I launched an ETF to track the Cheeseburger index, and charged, say, 3%? That’s an egregious fee, and is certainly not in keeping with the indexing’s roots. But this is how the industry has developed over the years – while some things have improved, others have grown worse. We recently wrote an article on index mutual fund managers charging over 2% for the S&P 500. 2%! For a passive index fund that has direct competitors at 0.05%!

On the other hand, there are plenty of “active funds” that are now priced well below 2%. Historically “active” funds have underperformed index funds due to their high cost. But now you have indexes that charge over 2%, active ETFs at 0.2%, and everything in between.

Now, let’s pull back a moment…

Am I arguing for active funds? Will you see anything in the video where I argue flatly for active funds and say there’s never any room for passive? No. Well, then am I arguing in favor of passive funds? No, again.

As mentioned a moment ago, “active” and “passive” have largely become devoid of meaning – the purity is lost. Labels, at this point, are useless. So I’m not arguing for or against either camp.

So then what is it, exactly, that I am arguing for?

Well, my oft stated belief is that the only thing that matters is total return net of all fees, costs, and taxes. (Obviously with risk taken into account.)

I don’t care if an investor attains these superior total returns through an index, or an active fund. We actually mention in the video that I prefer an actively managed index to avoid the pitfalls of index frontrunning. Let that melt your brain for a bit, and actively managed index, what box does that fit in! Total net return is all that matters!

After all, if you were the most diehard passive investor in the world, would you turn down, say, 20% returns per year if I told you the investment was an actively managed fund instead of a passive index fund? I would hope not…

Therefore, with maximizing total return in mind, my company manages both active and passive strategies where we feel appropriate. In our opinion, there’s room for both.

We’re not the only ones who feel this way. Even Vanguard, the most famous index shop on the planet, has more active mutual funds than passive! That fact always surprises people. And about a third of Vanguard’s total assets under management are active…so here is the literal founder of indexing (John Bogle who started Vanguard), being open-minded and finding value in a non-indexing product.

So if the “active versus passive” debate isn’t really about “active” or “passive,” then what’s the issue?

John Bogle said it best:

“The conflict of interest in the industry isn’t about indexing vs. active management. It’s cost.”

And we agree. Passive buy-and-hold is not the holy grail. Neither is active investing. Maximizing your returns, net of fees, is our holy grail.

So with all this in mind, let’s turn back to Mark and what I believe are the other two confirmation biases that are blinding him.

Mark runs the $3b Index Fund Advisors out of Irvine. They are a classic buy and hold Dimensional Fund Advisors shop which believes strongly in index funds. Mark does a good job of educating clients, has written a nice coffee table style book, and has a website packed with resources.

As I just explained a moment ago, you would correctly guess that I have no issues with Mark’s style of buy-and-hold indexing. After all, I run a global buy-and-hold passive index fund (more on this later). But we deviate when it comes to our allegiance to buy-and-hold.

I tend to be more open-minded, believing there are lots of styles and approaches that work in investing, like value, momentum, and trend following. Remember, my allegiance is to net returns, not a specific strategy.

Part of the reason for this is because we’ve featured lots of active managers on my podcast and blog whose careers and track records illustrate that active works. One example was Ed Thorpe. His performance record goes down as one of the highest risk-adjusted returns of all time – in 230 months of investing, Ed had just 3 down months, and all were 1% or less. No down quarters, no down years. Annualized, his performance was over 19%.

With evidence like this in front of me, though I believe passive index investing has many great features, I recognize and embrace that 19% returns through an active strategy is an amazing performance. So I am fully open to it.

With that in mind, my company, Cambria has both passive and active ETFs. Enter Mark’s confirmation bias #2.

Mark’s paper begins to analyze the suite of Cambria funds with this statement: “The table below details the hard costs as well as the turnover ratio for all 8 active ETFs offered by Cambria.”

Full stop.

Does Cambria even have eight active ETFs?

No.

HALF of the Cambria ETFs analyzed in Mark’s article are passive index funds.

The odd thing about this statement is that Mark knew this to be the case. It was a point I made in our debate (time mark 4:30) with Mark sitting only inches away from me.

Did he not hear it? Did he choose to not hear it? I don’t know. But he either he ignored it, and/or did no homework on Cambria when writing the article.

But if we assume that Mark did, in fact, hear my comment about half of Cambria’s funds being passive, why would he claim they’re all active? Well, it’s simple confirmation bias.

(By the way, Mark himself allocates to value, small, social, sustainable, and other deviations from market cap weighting, but doesn’t consider himself active. I find this to be a double-standard.)

Remember, there’s nothing wrong with being active, of course. I consider that to be a compliment. And after all, with the definitions of “active” and “passive” changing so much, who really cares about the label anyway? (Confirmation bias point #1 about purity.)

But if you get this basic fact check wrong when writing an article that calls out an industry colleague, how are readers to trust the rest of the article’s points? It’s just sloppy journalism.

Moving on…

The 3rd confirmation bias from which I believe Mark suffers, is that since Cambria is an “active” ETF shop, we must be marketing products that have higher costs.

To this end, Mark highlights the costs for Cambria’s funds, and mentions:

“On average, an investor who utilized an equity strategy from Cambria experienced a 0.60% expense ratio. Similarly, an investor who utilized a bond strategy from Cambria experienced a 0.60% expense ratio.”

Our fees are in line with the average ETF cost, which is half the cost of the average mutual fund. Cambria’s ETFs range in cost from 0.25% to 0.69%. Mark uses DFA funds that range from 0.08% to 0.73%. So, pretty similar.

So if Mark’s statement is accurate, what’s the problem? Where’s the bias? The problem with this is that the statement is woefully incomplete.

As I mentioned earlier, what matters most to me is total fees, including all costs. So, let’s look at how we both implement our strategies through managed accounts…

IFA’s average portfolio expense looks to be about 0.33%. Ours is about 0.55%. But Cambria charges a separate account management fee of 0%, with a technology platform fee of 0.15% from Betterment (and no trading commissions). Our Fidelity offering is 0% across the board, but includes commission costs.

IFA, on the other hand, charges a sliding scale of fees. It starts at 0.9% plus trading commissions of $10-$40 per fund. So, doing the math, that’s 0.90% management fee + 0.33% fund expenses = 1.23% total fess, plus trading commissions. (By the way, for smaller accounts, commissions can be even more important than management fees. Using $20/trade for 12 funds, that’s $240 for a $100k account, or another 24 bps for every trade!)

So, let’s bust Mark’s confirmation bias #3: Despite the fact that I’m an “active” manager as Mark suggested in his article, and active shops are most likely pushing higher-cost products/services, our total Cambria fees are about half of what IFA charges. Obviously, this fact doesn’t fit the overall narrative of “active is more expensive.” Even worse, it seems to run counter to Mark’s narrative of “passive indexing is inexpensive.”

But that is not even the best comparison with Mark’s buy and hold allocation, as our separate accounts include tilts to value, momentum, and trend. So, let’s try to compare apples to apples.

Cambria manages a global buy-and-hold asset allocation ETF. It is the first (and as far as I know, still only) ETF with a permanent 0% management fee.

All-in, this passive index fund (again, note “passive” which busts confirmation bias #2) costs just 0.25% (this 0.25% cost stems from some of the underlying ETFs in this fund of funds). Both IFA and Cambria are offering similar global, buy-and-hold allocations with tilts to value. Yet, in this case, IFA is literally almost FIVE TIMES AS EXPENSIVE.

Why doesn’t Mark mention we run one of the cheapest global asset allocation index funds in existence, and his firm is so much more expensive? Did he not hear me? He must’ve, since I discuss it at length for a few minutes (look around 14:45). The reason is because a bias is colliding with facts, and when someone isn’t willing to revisit that bias, those facts must then be either destroyed or ignored.

Let’s pull our heads out of the details for a moment and look at the industry at large. It may help explain why my company and I were on the receiving end of such poor journalism and analysis.

Expensive passive buy-and-hold index products are going the way of the dinosaur. Downward pricing pressure is going to kill any shops that refuse to join this race toward the bottom.

Now, this is a great evolution for investors. We’ve written about this many times over the years including recent articles “All the Fees in the World” and “The Cheapest Portfolio in the World“. But it’s challenging to the “old school” way of investment product pricing.

Mark utilizes reasonable indexing products. But those reasonable products come at higher all-in costs when you tack on IFA’s fees. Cambria and Schwab have now set the floor for this type of separate account asset management offering at 0%. It’s basic fiscal Darwinism – when some groups are charging 0% and you’re charging 0.9%, you’re not going to survive. (Note to financial advisors: this fee destruction is referencing pure asset management. We’ve said for a long time if you offer additional value added services you can we worth that 1% and your weight in gold, but the value is not in the asset management side…)

You can look for boogeymen and/or someone to blame (smart beta strategies and active investors), or you can be willing to challenge your own fundamental belief, and reevaluate your own biases.

Active and passive are both great strategies, and both have roles in a portfolio. But what factor trumps each? Fees – and how those fees affect your net returns. This is truly all that matters.

So, what’s the takeaway for readers in all this as they wonder about their own sacred cow investing beliefs, the active versus passive debate, the indexing versus smart beta argument, and so on?

Well, I think Mark has great advice. He concludes his article with:

“Similar to the fate of other investment firms, the market as a whole is more informed than any single individual. Competition in the industry has removed almost all opportunity to find risk-free value that can be reliably captured. A better solution is to align yourself with the market instead of against it and buy, hold, and rebalance a globally diversified portfolio of index funds.”

This is a conclusion with which I agree! His global, buy-and-hold asset allocation is a reasonable allocation. But if you’re an evidence-based investor, and believe in Mark’s advice, then you should follow that advice via a cheaper alternative. There are plenty of DFA firms that have a less expensive fee structure than IFA.

Or, for a similar allocation, Cambria offers a buy-and-hold, rebalanced, globally diversified portfolio of ETFs (GAA) for 0.25% all in. Heck even Vanguard, Schwab, Betterment, and Wealthfront roboadvisors have similar offerings for around 0.5% all-in. And these offerings also offer tax harvesting (and don’t invest in tax-inefficient mutual funds). For comparison, Mark is at 1.23%, two-to-five times as expensive…

Let’s wrap this up…

We’ve all heard the phrase “the end justifies the means.” Friends, “active” and “passive” are not the “end.” Frankly, they’re not even the real issue in all of this. The issue is what does each of us do when we face market realities that challenge our core beliefs?

Are you like the cop from South Park, unwilling to believe something outside your favorite narrative? Are you too rigid to challenge your own world-view?

Not one of us gets it right all the time. We have to be willing to grow, change, adapt, and admit prior mistakes of strategy and implementation. Why? Because our allegiance should be toward growing wealth – not a market strategy.

Keynes might have said it best: “When the facts change, I change my mind. What do you do, sir?”