If you enter the phrase “dividend investing” in Google, how many entries do you expect you’ll get?

I got 57 million in 0.60 seconds.

A search for “dividends” on Amazon returns a whopping 8,000 books, with exciting titles such as “Get Rich with Dividends” and “How to Supercharge Your Investment Returns with Dividend Stocks.”

And if you type “dividend investing is…” into Google, its autofill feature will pop up, providing you various phrases it believes you might be typing. The list is mostly all positive, with the top autofill option reading: “Why dividend investing is superior to growth.”

All this underscores a reality: most investors love dividends, which is why what I’m about to write is so awkward…

They’re making you poorer.

In a taxable account dividends could have cost you anywhere from 0.3% to over 3.0% in returns PER YEAR since 1974. If your goal is optimizing your returns, then a blind allegiance to dividends could be a very, very bad idea.

To make sure we’re on the same page here, let me catch everyone up.

About two months ago I wrote an exploratory blog post titled, “What You Don’t Want to Hear About Dividend Stocks” which called into question dividend investing. While I expected a large amount of hate mail, the post was actually very well received.

In the article, I set out to examine if we could build a better investment strategy by avoiding dividend stocks. The reason being dividends are taxed every year whereas capital gains are only taxed when a position is sold. So if one could find a strategy that avoids dividend stocks yet replicates their returns, a taxable investor would realize higher returns by not having to pay Uncle Sam every year.

My original post found that by applying a simple value strategy, an investor could indeed approximate the returns of dividend investing. This meant that, yes, there was an after-tax benefit to choosing a value strategy over a dividend strategy. But the numbers actually provided a takeaway I wasn’t expecting.

It turns out that the simple value strategy (which included avoiding high yield stocks) actually produced higher returns than the dividend strategy—not just similar returns. In other words, before we even get to the tax benefits, “value” had already trumped “dividends.”

It was an interesting reminder that while many investors use “value” and “dividend” investing interchangeably, they’re unique strategies with value being superior.

I had worked with Ned Davis on the research, but we were limited by our database to only going back to 1995. To test these results with a larger data set, I partnered with our old friends at Alpha Architect Wes Gray and Jack Vogel. We examined this strategy all the way back to 1974. And the results are quite stunning.

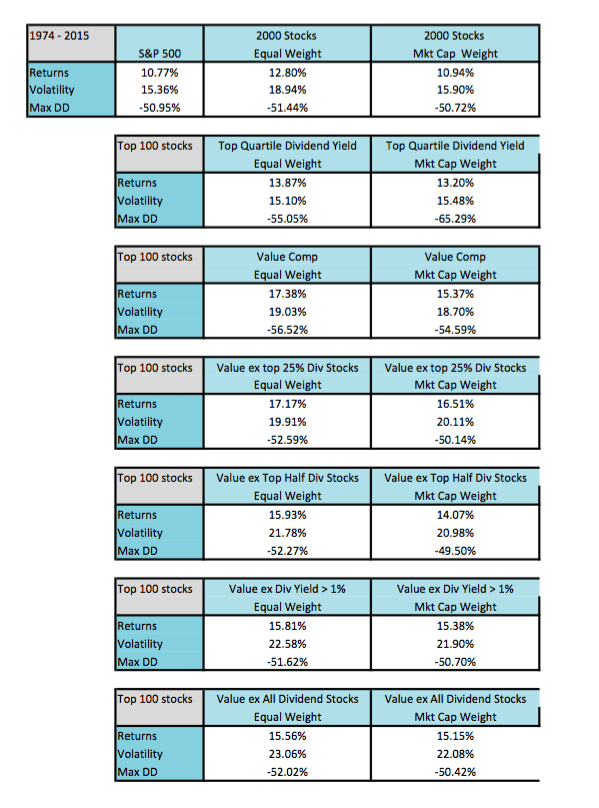

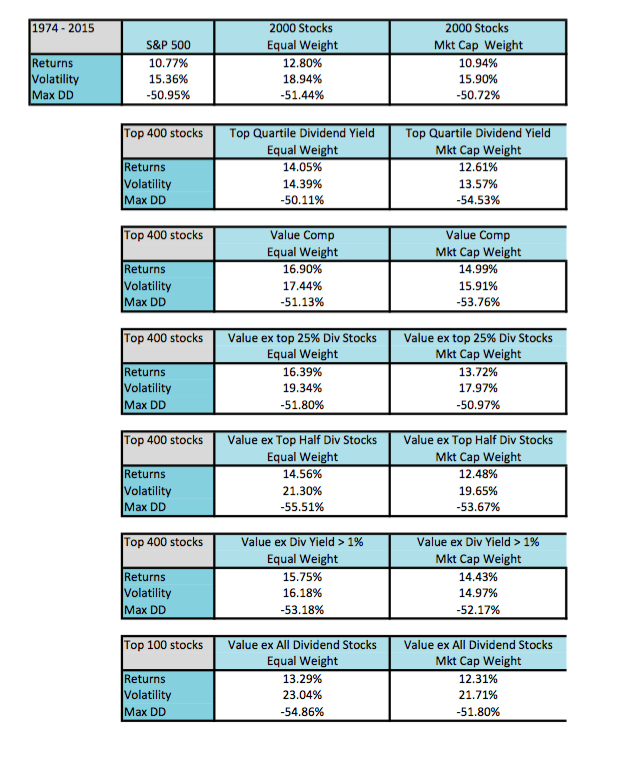

Below are two tables. The first table examines holding 100 stocks, the second examines 400 (both out of a universe of 2000).

The first row shows the S&P500, and the equal weight and market cap weight of the top 2000 stocks. Notice that the market cap is near identical to the S&P500, and also that the equal weight is about two percentage points higher than both (one reason we always say to avoid market cap weighting).

The next row is taking the top 25% of the universe by dividend yield. Notice this adds about a percentage point over buy and hold.

The next row is weighting stocks by valuation. One can define “value” any number of ways. For our purposes today as in our original post, we constructed our value composite by taking the top stocks by a combined rank of price-to-earnings, price-to-sales, price-to-book, and EBITDA-to-EV.

Notice the massive outperformance over the broad market and the dividend portfolio. This verifies the takeaway from our original tests: Focusing on value is a much better value strategy than dividend yield!

We then examine a few strategies of avoiding some to all of the dividend stocks. First is avoiding the top 25% highest yielders, then the top half, then all with a yield over 1%, then all dividend stocks entirely.

Top 100 stocks (more concentrated)

Top 400 stocks

Note that nearly ALL OF THE VALUE STRATEGIES beat the dividend strategy (which just accentuates the distinction between value and dividends). So, again, before even bringing taxes into the picture, value has outperformed dividends. These numbers are all ignoring taxes on dividends.

But let’s now include the tax-effect. While those fat 4%, 6%, 8% or even higher dividend yields sound great, realize you have to pay taxes on that income every year.

We ran two estimates with real historical tax rates at the lowest and highest tax brackets, and found that the benefit of avoiding dividend stocks ranged from an after tax bump of 0.3 to over 3 percentage points PER YEAR.

Many investors, including retirees, value those dividend checks they receive every quarter. But this research reveals that those dividend checks carry a huge opportunity cost. Your “bird in the hand,” so to speak, is costing you about three or four in the bush.

So there are two things to do with this. One, if you’re an income investor enjoying on the cash flow from dividend stocks, put those investment in tax deferred accounts or consider whether you can meet your cash flow needs some other way. If so, then reallocating toward a low-dividend value strategy should increase your overall returns.

Second, if you’re a dividend investor because you’ve been under the impression that dividend investing (and reinvesting those dividends for compound growth) is superior, it’s time to rethink that. When you factor in the tax implications of dividend investing versus a low-div value strategy, the difference in returns is striking.

Sure, investors love dividends, but maybe they’d love them less if they understand how expensive dividends really are.