This excerpt is from the book Global Asset Allocation now available on Amazon as an eBook. If you promise to write a review, go here and I’ll send you a free copy.

—-

Harry Browne was an author of over 12 books, a one-time Presidential candidate, and a financial advisor. The basic portfolio that he designed in the 1980s was balanced across four simple assets, and you can see Harry explain the theory here:

“For the money you need to take care of you for the rest of your life, set up a simple, balanced, diversified portfolio. I call this a “Permanent Portfolio” because once you set it up, you never need to rearrange the investment mix— even if your outlook for the future changes. The portfolio should assure that your wealth will survive any event — including an event that would be devastating to any individual element within the portfolio… It isn’t difficult or complicated to have such a portfolio this safe. You can achieve a great deal of diversification with a surprisingly simple portfolio.”

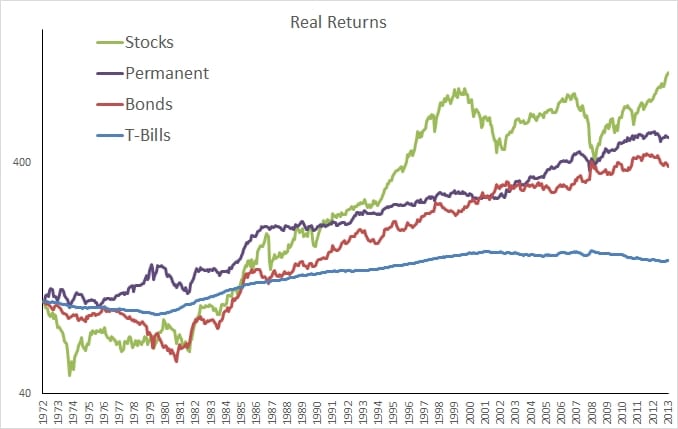

Although the portfolio underperformed stocks, it was incredibly consistent across all market environments with low volatility and drawdowns. This presents a classic dilemma for investors, particularly professional advisors. What is the trade-off for being different? Despite the incredibly consistent performance there are many years this portfolio would have underperformed U.S. stocks or a 60/40 allocation. Can you survive those periods even if you believe this portfolio to be superior? See Figure 28.

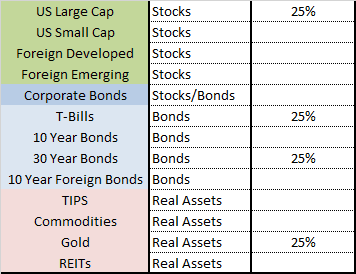

FIGURE 28 – Permanent Portfolio

Source: Browne

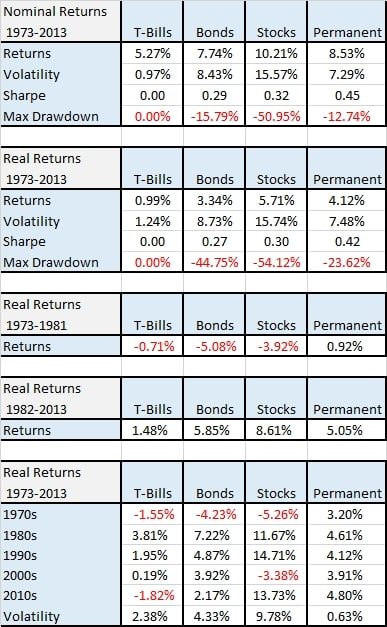

FIGURE 29– Asset Class Returns, 1973-2013

Source: Global Financial Data

Next to Marc Faber’s allocation that we profile later in the book, this allocation has the highest weighting to gold. Gold is an emotional topic for investors, and usually they fall on one side or another with a very strong opinion for or against. We think you should learn to become asset class agnostic and appreciate each asset class for its unique characteristics. Gold had the highest real returns of any asset class in the inflationary 1970s but also the worst performance from 1982 – 2013. However, adding gold (and to a lesser extent other real assets like commodities and TIPS) could have helped protect the portfolio during a rising inflation environment. Gold also performs well in an environment of negative real interest rates – that is when inflation is higher than current bond yields.

The next portfolio we look at just aims to be average, and it turns out that isn’t a bad thing.